New York, USA – April 23, 2020 – Latest analysis from the CEPRES Investment Platform highlights major sectors that could be winners and losers from the Coronavirus crisis. By evaluating current value creation and revenue growth opportunities in PE-backed companies and contrasting with the GFC (Global Financial Crisis) period the CEPRES Platform is able to identify potential outcomes from the COVID 19 crisis.

The results were based on deep analyses of 80,500 deals from across 7,800 funds and encompassing over $28 trillion worth of PE-backed companies. One part of the analysis looked at the growth of revenues and EBITDA before during and after the GFC across different sectors and developments before the COVID 19 crisis. This was then combined with how allocations have shifted and more recent growth prospects from the most recently reported operational data in CEPRES.

Key findings shared by CEPRES:

Most traditional, and especially manufacturing businesses, with global supply chains, have a high risk for slow and weak recovery. This is because of the unique nature of the current crisis, but also systematic market risks that have been developing in these sectors over the last 24 months (ref CEPRES paper on How to identify & avoid systematic risk by Dr. Daniel Schmidt, BAI AIC Conference_,_ May 2019).

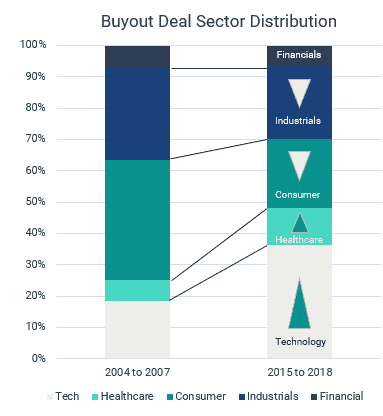

Shifts in PE sector allocations post-GFC have helped reduce the impact of this supply chain-dependent business exposure on LP portfolios. Traditional industrials and consumer allocations reduced from 75% pre-GFC to 50% pre-Coronavirus Crisis, however still major parts of the portfolio will be heavily impacted.

Traditional businesses in markets with strong domestic consumption will recover faster and benefit in the mid-term.

Emerging market investments will be exposed to a higher systematic and geopolitical risk, but those with digital reach are less correlated to likely increasing geopolitical tension caused by concerns over the movement of people and anti-globalization sentiment.

For Digital driven companies, and Technology, Healthcare, and Financials sectors we generally expect to benefit and recover sooner to as strong as their pre-crisis level and therefore positively balance overall portfolio performance. Deal Activity will increase in those sectors and valuations accelerate. This is both driven by the unique nature of the crisis leaning heavily on these sectors, but also pre-crisis resilience and growth prospects, especially for Technology and Healthcare.

There will still be some losers in Technology, Healthcare, and Financials where idiosyncratic exposure to the COVID-19 Crisis will adversely impact. For example Technology businesses related to live entertainment, film production, and events, in Healthcare social care facilities and dental practices, and in Financials Life insurers with high liabilities could all be adversely affected.

Source: CEPRES Platform Copyright © 2020 CEPRES GmbH

Source: CEPRES Platform Copyright © 2020 CEPRES GmbH

Commentary:

“Having learned from the last financial crisis in 2008 and established relevant systems and processes, central banks and governments were much faster and aggressive on both sides of the Atlantic to back the economy with massive stimuli in the last weeks. That will help drive a faster recovery for healthy businesses and boost deal outcomes afterward with positive money multiple return effects. That reduces the likelihood of a double-dip pattern with the intensity seen during the GFC. This level of stimulus will be limited to larger economic areas where such quantitative easing does not lead to a sudden overinflating of currencies or risk of State bankruptcies. “

Dr. Daniel Schmidt, Founder, and CEO